Good morning. I have been working with a Landman to work on the details of a sale and not sure what a fair price is for the property. There are several areas they are looking at with fractional shares in them. Any chance someone can tell me what a fair price per net acre would be for these areas? Any help would be very appreciated.

Also trying to understand how some of the people I have seen comment on things here in NM like NMOilboy or CMC15 identify how they can track the location of horizontal wells?

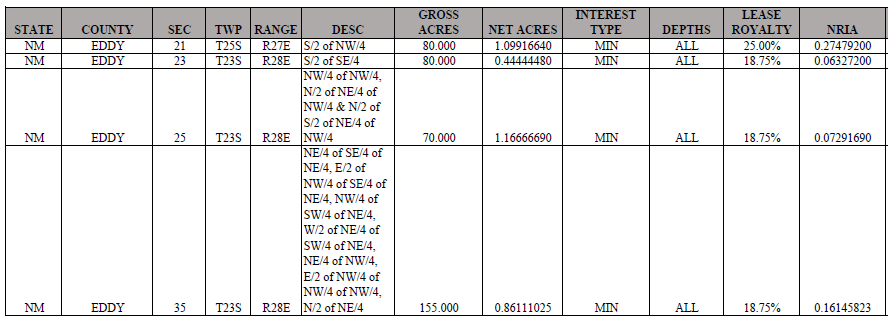

Real quick, is the NRIA calculation yours or the landman’s? I’ve not personally seen that acronym associated with that calculation, but I could maybe POSSIBLY see the use of it…maybe? The definitions I’ve commonly seen call it NRA and it would be higher than a NMA if greater than 1/8th lease royalty as it assumes 1 NMA = 1 NRA at 1/8th royalty.

NRI means something different in the industry (net revenue interest; typically used by WI owners and it’s approximately working interest times [1 - Lease Royalty]) and is not typically displayed in a net revenue interest per acre format…but that’s what this looks to be.

NRIA is the move that some folks, Viper for one, use to normalize royalty/ORRI/NPRI interests. An NRA is an interest that is equal to what you would have if you had a single acre at 1/8th royalty. An NRIA is equal to the interest in a single acre at 100% royalty.

So if you have a 1% ORRI on 100 acres, you have 1 NRIA. And 8 NRA. Mostly it seems like a way to trick people into getting a huge offer per “acre.” As if anyone in the mineral business would besmirch their honor. So this is 1.636 x 8 NRA = 13.1 NRA.

Ideally everyone knows the deal and it doesn’t matter if you are talking NRIA or NRA, what you own is what you own and you can translate across definitions. But most people talk in NRA, for sure.

NMLobo:

What is a fair price? Talking in NRA in the current environment:

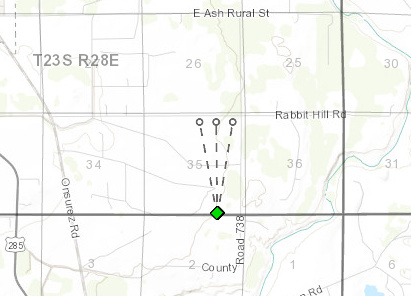

I’d guess that the 23S28E stuff, mostly being in Section 35 under Mewbourne, is worth around $9k/NRA. The small interest in Section 23 and 25 under Chevron is probably $13k/NRA. 25S 27E is probably $7k/NRA. So what does that make it, something like:

That’s not gospel or anything but that’s a guess +/- $20k on what a reasonable transaction price would be currently. I may be out of touch and there are a lot of people whose version of reasonable is different, so who knows. Mostly comes down to whether or not you think Mewbourne will drill upper Wolfcamp laterals in the Layla (Section 35) unit. As far as telling where Horizontal wells are located, I am basically cheating by using software at work that has well surveys in it. Drillinginfo or IHS.

The info provided on that excel sheet was prepared by the landman. I was very unfamiliar with it as well and did a lot of research to make sure I understood what they were doing with that computation. I am guessing it is a way for companies purchasing property that is already under a lease to get a better long term price based on the economics they are already under. Maybe it is a way to see a fractional share and not need a bunch of additional info like a lease. I am certainly new to this whole process but have learned a lot. Thanks for the input!

Thank you for the info and feedback, very helpful in getting comfortable with everything. How do you go about determining if Mewbourne will drill the upper Wolfcamp area or not? If they do decide to drill, would those areas be something you would say keep or sell if the pricing is right? I know there is almost always a better financial payout long term if the lease rate is appropriate but not sure how to weigh the options with selling versus leasing later.

If I do end up making a deal I will certainly post the info here, this place has really helped me understand a lot about oil and gas and what to do with interest in minerals when you inherit them.

How do you go about determining if Mewbourne will drill the Upper Wolfcamp or not?

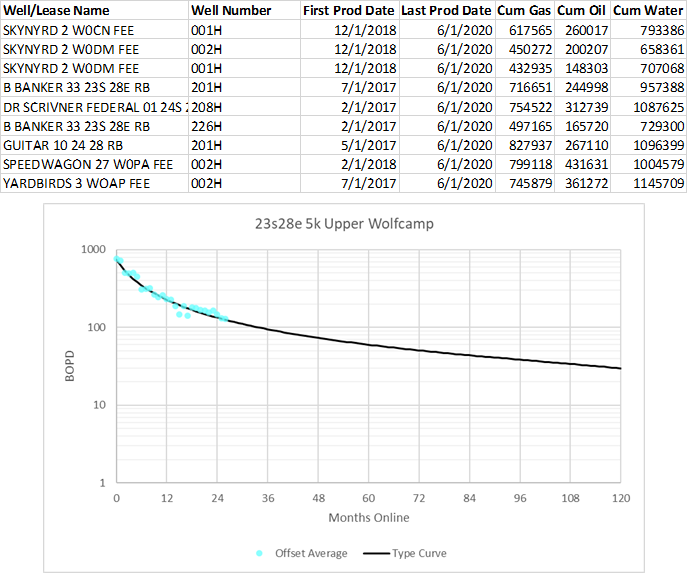

If it was me, and I was feeling crazy and I had a DrillingInfo subscription:

Look at offset well production for wells like the ones that might get drilled here. Let’s say that perhaps these wells are all nearby Upper Wolfcamp producers, and that their average historical/forecasted production looks like this:

Those are pretty decent wells. Expected total oil recovery of > 400,000 per mile long well.

Then you stick that flowstream into an economic model, say one that assume a 5000’ lateral costs about $5.5m to drill and complete. And other associated assumptions. At $40 oil, that potential well is something like a 15-20% IRR BTAX to Mewbourne. That probably will not get drilled. At $55 oil, that well is something like 40% IRR BTAX. That well almost assuredly will get drilled (in some timeframe). At least that is my guess. So, IMO, if oil price goes up, there are at least 4 more upper Wolfcamp wells to drill here. (In addition to some other possibilities). If oil stays low, then like EVERYWHERE, its probably going to be tough times for people waiting to see if wells get drilled.

Currently Mewbourne is running 3 rigs in the Delaware and they are in better places (26S29E, 25S28E) or similar places (23S34E) to this.

I think I’d keep this if some of these are true:

You are bullish on oil prices

People are offering you sub $100k for all of it

It has some extreme sentimental value

$100k here or there doesn’t matter all that much

There is some thrill to getting checks in the mail each month and seeing what happens

Reasons I might sell:

You figure oil is roughly equal to thermal coal and everybody is driving an electric car in 10 years

Keeping track of small checks and details on this over 20 years sounds like a pain, not a thrill

People are offering you over $110k for it

You’d rather somebody else deal with the risk/reward of possible development

There aren’t a lot of wrong answers IMO once you remove getting completely hosed on pricing out of the equation.

Looks like the land is private. We just have the mineral rights in an NPRI for what appears to be about 200 acres north of Frightened Turtle (FT) well and south of the three Peregrine wells. Township 24S, Range 34E, Section 34, NE/4 and NE/4 SE/4. Now I notice a 4th Peregrine and they were all showing as “cancelled” just over a week ago, today they are all listed “New.” They are all horizontal and operated by EOG. Offer was made by Regency O&G. They want an outright purchase/transfer of all rights/interests. Are there any resources to determine what a ballpark fair price should be?

I apparently have in Eddy County, New Mexico SEC 34, T22S, R27E. I have called the operator of the land, which has wells, for more information, to no avail. These are basic questions, but I could really use the help:

How do I access documentation that I have this land?

Should I have been receiving royalties from the operator for the past 11 years?