Hello,

New to the site and seeking information on 2-15N-12W. It’s currently leased but production is lessening each month. Getting substantial offers to sell.

Thank you in advance.

Hello,

New to the site and seeking information on 2-15N-12W. It’s currently leased but production is lessening each month. Getting substantial offers to sell.

Thank you in advance.

Hi Jfaust,

Horizontal wells are notorious for their high initial productions and steep declines; more wells (increased densities) can offset that decline and provide more income. There have been multiple location exceptions and a few increased density orders just to the south of you - which is likely why you are getting new offers to sell. It looks like there are multiple OCC applications pending as well. Selling minerals depends on your investment horizon and personal situation.

Best of luck!!

Unless your statement is limited to the decline in initial cash flows from the first well in a unit, then you might want to reflect a little more on the subject.

Increased density drilling (more wells) does not offset decline rates, it actually can make decline rates worse due to interference between the well bores.

This has been witnessed across the STACK/SCOOP as well as other basins. Furthermore, ‘parent wells’ can be significantly impacted if the operator does not take precautions such as pressuring up the parent well prior to fracking offsets, and the efficacy of the process is not certain.

Seems likely. Alta Mesa recently drilled and fracked 3 more wells on the same pad as our existing well. They evidently halted production on the existing to protect it so no royalties for several months. Then production started coming back slowly but is far less than it was originally. The 3 new wells spud in July so don’t expect any production results on them until next January or February. Have no idea what will happen with 4 wells producing from same pad. Their plan is to put down 3 more but I suspect it will depend on what the current wells do. All are horizontal wells. Production on the first/original well was about 500 bbl. I don’t think we’ll be getting rich! LOL.

Very good point. Yes, my statement was limited to increasing cash flow from more wells being drilled in that unit - not offsetting wells. Offset wells completed to the east or west of a producing well will almost certainly frack into the parent well. From what I understand, most horizontally-targeted reservoirs in the Anadarko Basin have fractures oriented east-west, so a child well completed east or west of a parent well will frack into the parent well and cause oil and gas production to decline or cease, and formation water to increase for a few months.

Frac hits are a clamant problem in both conventional and unconventional (“shale”) plays. I am in a few wells that have seen water production increase up to 8x while oil and gas drop 90-100% from their engineered declines, however they have recently recovered back to their pre-frac decline after a few months. The magnitude of the effect is dependent on multiple variables.

In the OP’s case, one should research wells being drilled around them and compare production. The well he is currently receiving income from might have been fracked into and it might be an increased density candidate, thus, 2-3 months of production anomalies shouldn’t dictate a decision to sell. IMO, the above points, and many others, should be taken into account before selling.

Last I checked, there were over 25 cases of frac hits being so powerful that it caused fluids to purge up an offset well tubing, polluting the well site - some wells were more than a mile away from the well being fracked.

I have been following some of Alta Mesa’s downspacings and most of them recover from a frac hit but the hit will definitely affect the wells for some time. I’m sure you’ll be all right. DM me if you think otherwise ![]()

Thanks for the info. I had planned to sell early last year when I got an acceptable offer, then it got complicated when the buyer didn’t pay within a month and they reneged on the original offer so I decided to forget about selling when I found that 6 more wells were planned. Now I figure I’ll just sit back and see what happens when the completion reports come in.

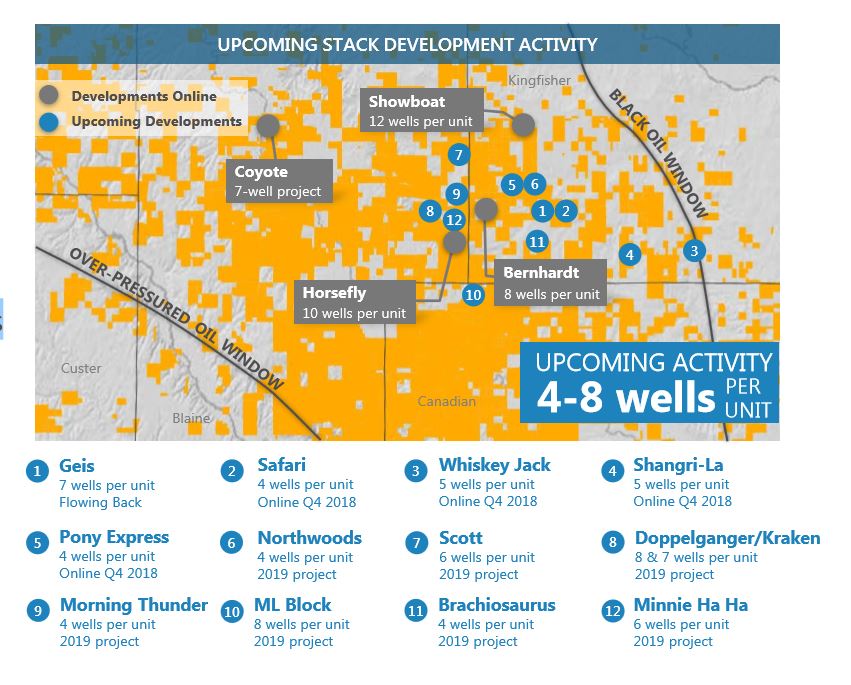

Per DVN’s Q3 operations report:

Pilots testing higher-density spacing not optimized — Showboat upside test underperforms vs. plan (12 wells/unit) — Horsefly delivered improved results (10 wells/unit) — Bernhardt rates limited by flowback strategy (8 wells/unit) — Lighter-spaced Coyote project delivers best results

Learnings from high-density infill tests — Initial results indicate spacing was too tight — Flowback approach key for oil recoveries — Upper Meramec delivered best well results — Vertical communication observed — Substantial D&C savings achieved (pg. 15)

Reverting to “base case” spacing to optimize returns — Upcoming activity targeting 4-8 wells per unit — Well placement focused in Upper Meramec — Flowback adjusted to improve performance

Project IRRs to benefit from less capital intensity — Utilizing tailored, more capital efficient completions — Projects to benefit from less infrastructure capital on centralized facilities

Similarly, NFX was under pressure due to underperformance in the STACK. This is not uncommon throughout shale plays, but the Mid-Continent’s expectations were pushed pretty high, and still are pretty high. Companies simply can’t deliver their type curves across a tightly spaced multiple well unit consistently. This will eventually impact mineral values in multiple ways. Not only will production projections be reduced, and hence projected cash flows go down, but the overall allocation of capital and velocity of development will start to pull back as companies look to allocate capital to higher value plays. Add in the dramatic retreat in oil prices from the mid $70s to the low $60s and there are many mineral buyers licking their wounds and crying tears of the winner’s curse for their overly optimistic estimates, and many mineral buyers that might have missed peak pricing as the buyer pool shrinks. Of course the pendulum can swing the other way on pricing again, and it will, but always remember there is only so much oil and gas in a formation, and as important, only so much formation energy available to produce those hydrocarbons.

DVN 2018 11 NOV Q3-2018-DVN-Operations-Report-FINAL.pdf (1.5 MB)

Yep, we have old vertical wells that have been producing for more than 60 years. Of course it’s just a trickle now and horizontal wells are going in around them, so surprised that they still produce anything.

John - main problem is the over optimistic assumptions everyone likes to use. You see it in every play. Initially everything is great, and the belief and hype spreads like wildfire. Then cracks start to appear in the story, and eventually there is a huge negative overreaction. Eventually people will realize that there is a true core, and that spacing is significantly more moderate than initially hoped but still better than previous times.

True. I guess that whole law of diminishing returns kicks in at some point when drilling so many wells into a limited reservoir. Alta Mesa had to revise their FY2018 production down by around 2,000 boe/d due to frac hits and shut-in times on pad drilling. I believe they will have to revise some of their SEC PDP, EURs, and type curves for the same reason. A close look at their 10-K and 8-Ks tells a developing story in regards to shut-ins and frac interference.

Trying to time mineral purchases when oil is high and production is flush could be considered gambling, not investing, in my opinion. I am still waiting for an institution to offer hedges for (smaller) mineral owners, but the obvious problem is collateralizing a mineral owner for their hedge—and volume is a problem too, of course. This collateralization process is one reason why I think Viper Minerals has been successful and why Continental and others are getting into minerals.

In one of the sections I am in, there are two vertical wells that combined produce 12-15 bopd and 20+ mcfd after approximately 10 years of production. These wells are spaced on a 320-acre unit, so the royalty owners are still receiving more in cash flow than a majority of mineral owners owning the same number of acres but with horizontal wells spaced on a 1,280-acre or even 640-acre unit that have been producing for 5+ years. Vertical/conventional production shouldn’t be completely written off just yet as most are spaced on 40-160 acre (1/30th to 1/16th the size of major horizontal units) units and therefore produce similar cash flows as they enter terminal decline. And they’re far cheaper to operate.

Yes, earlier this year there was fracking going on near our first horizontal well and production went to zero. It stayed that way for several months and Alta Mesa kept saying they hoped things would come back but no time frame. When it did start coming back it was something like 20% of original, then it increased a little (not much). Now I should have another royalty check within a week to see if things have improved at all.

With all the reports that I see I wonder if the higher density is really such a good idea although the companies always say (in their requests) that they need additional wells to adequately recover the oil in the pool. As for high expectations, yep, I’ve experienced it. Last year when I was considering selling I got some pie in the sky offers, even the one I accepted went down the drain. The buyer sat on the sale for a month until I started bugging them and then they said the oil wasn’t as good as they predicted so they wanted to back out and make a much lower offer. I basically let them know where they could stick it.

Regardless of what happens I’m fine with just keeping everything and waiting for the results from the new wells. I’m pretty much turned off on selling, definitely don’t trust some of these people including the landman I had working for me.

Who was the “buyer” John? Wonder if it was BCF. I had a bad experience with them.

Not BCF. Mahan was the name of the fellow supposedly fronting for an investment group but have no idea who the actual people were other than the landman I hired said they were reliable and well-funded which turned out not to be the case. I wouldn’t do business with Mahan or the landman again. I won’t give the name of the landman since he was referred by someone else and I don’t want to get them into a bind since I know they are reliable people who just happened to refer me to someone who wasn’t.

John, what area are you talking about? We have some in Section 18, Township 16N, Range 13W and in Section 4, Township 17N, Range 12W. No contacts for several months but now getting a few offers. Do you know anything about Long Point Energy out of Dallas, or MayHawk Energy?

Larry, I haven’t gotten any offers recently for that area (Section 4, Township 14N, Range 12W and Section 33, Township 15N, Range 12W), but just recently got Multi-Horizontal Well documents filed by Continental Resources, so there is definitely activity in the area. I sold my sister’s interest in this area last year via auction because I have been appointed her Guardian.

I know someone that used to work at Alta Mesa (looks like they just went through some pretty big layoffs and they are actually no longer there). Anyways, I don’t think Alta Mesa is really that involved in Blaine (I know they are in Major and Kingfisher). After seeing this discussion I talked to my Alta Mesa contact and he did say what has been mentioned in this thread: they are decreasing the number of wells that they predicted could fit in a section (from over 8 wells to closer to 4) so they think they will ultimately not be able to produce as much oil. I recently talked to a few mineral appraisers that I found through Google and mentioned this to them. Some seemed to be aware of this problem but most kept telling me that they think that companies can fit 8 to 12 wells in a section, which does not seem to be the case. I am looking to get my minerals appraised so I from an appraisal standpoint I would rather they value the property as if there was a lot of wells in a section. But it is also making me think I should sell my minerals sooner rather than later before the entire industry catches wind of these problems and adjust their unrealistic expectations. Anyone else having these thoughts?

Interesting to hear your inside info. We have various interests in Kingfisher County and one is with Alta Mesa. I was enthused when they planned to put 7 wells in one of our sections after they had completed the first well. Unfortunately the first well was disappointing and much less than predicted, then they drilled 3 more but they haven’t released results on them yet but they did put plans for the additional 3 on hold which doesn’t sound very good. I also noticed that some people have left Alta Mesa but didn’t know the reason so interesting to hear you say they had a layoff. Kinda seems like their wells are just not paying off.

The industry is well aware of the parent-child interaction situation. They are doing quite a bit of research and testing to see what the best solution is on a reservoir by reservoir basis. In some areas, where there are multiple horizons, they may try a “wine rack” approach with four to six wells per reservoir per section staggered to take advantage of the best drainage patterns. Other areas with only one reservoir will most likely have less wells, but it would depend on the reservoir and whether it was primarily oil or primarily gas. Horizontal drilling and production is still fairly young in its technical life cycle compared to over a hundred years of vertical drilling so they have a lot to still figure out. The recovery factors are still fairly low in shales, so there are a lot of hydrocarbons left in the ground for the future.